Colliers Report: 2021 will see stabilization and improvement

February 2, 2021

Research & Forecast Report

2020 SOUTH CAROLINA | HOSPITALITY

Key Takeaways

- With the availability of the new COVID-19 vaccine, occupancy and revenue per available room (REVPAR) is anticipated to increase.

- The passage of the COVID-19 Relief Bill at the end of 2020 should provide financial stabilization to hotel properties.

- There will be a tourism boom beginning in the fall of 2021 as the vaccine is fully deployed and households begin spending their savings.

- With the improvement of market fundamentals, transactional volumes should increase over the next year.

For additional commercial real estate news, check out our market reports here.

South Carolina Market Overview

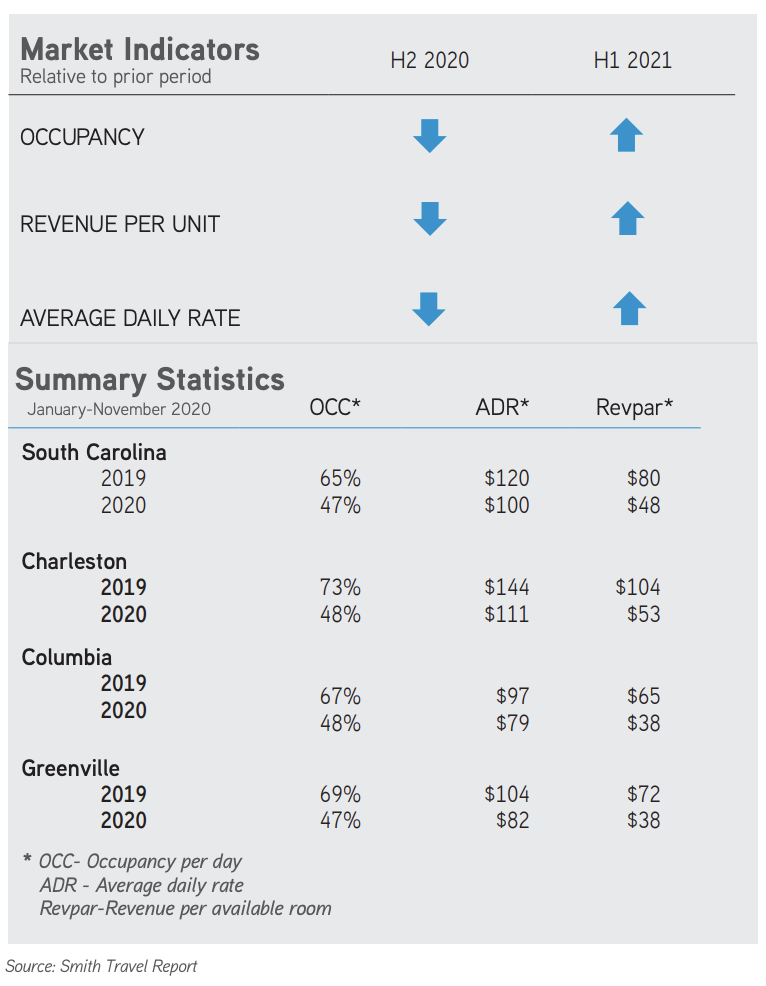

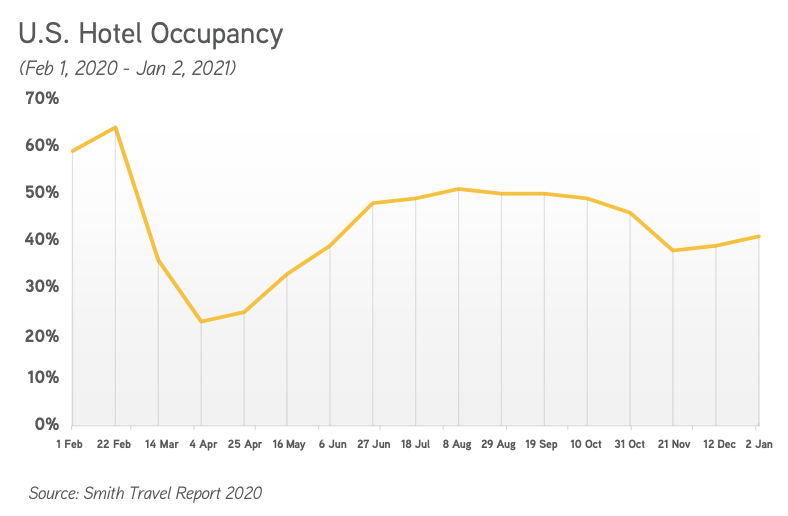

The hotel sector was negatively impacted across the nation in 2020. Occupancy dropped to nearly 20% in April, recovered to 50% and slowly fell back to 40% as the number of cases surged in November and December. In South Carolina, occupancy dropped to about 50%, the average daily rate (ADR) was reduced by 17% and revenue per available room was halved. Geographically, results varied substantially. Drive-to markets like Myrtle Beach, Hilton Head and Charleston outperformed similar fly-to markets. Similarly, economy and mid-scale properties with fewer amenities and limited convention and meeting space performed better.

The hotel sector was negatively impacted across the nation in 2020. Occupancy dropped to nearly 20% in April, recovered to 50% and slowly fell back to 40% as the number of cases surged in November and December. In South Carolina, occupancy dropped to about 50%, the average daily rate (ADR) was reduced by 17% and revenue per available room was halved. Geographically, results varied substantially. Drive-to markets like Myrtle Beach, Hilton Head and Charleston outperformed similar fly-to markets. Similarly, economy and mid-scale properties with fewer amenities and limited convention and meeting space performed better.

Operationally, the hotel industry was one of the most adversely impacted over 2020. There were two pieces of legislation passed in 2020, the  CARES Act and the COVID-19 Relief Bill to address this. Both provided funds to small businesses in various forms to offset the negative impact of government shutdowns and reduced economic activity. Each materially impacted the hotel industry with low interest and forgivable loans. However, the health of hoteliers varied substantially depending on the mix of properties and rooms within their portfolios and their relative financial position prior to the pandemic. Operators whose mix of income was dominated by upscale, upper-upscale and luxury properties lost the most business and had the largest ongoing expenses to continue to operate. Conversely, operators whose income was generated by economy, midscale and upper midscale properties fared much better with lower operational costs and greater occupancy levels.

CARES Act and the COVID-19 Relief Bill to address this. Both provided funds to small businesses in various forms to offset the negative impact of government shutdowns and reduced economic activity. Each materially impacted the hotel industry with low interest and forgivable loans. However, the health of hoteliers varied substantially depending on the mix of properties and rooms within their portfolios and their relative financial position prior to the pandemic. Operators whose mix of income was dominated by upscale, upper-upscale and luxury properties lost the most business and had the largest ongoing expenses to continue to operate. Conversely, operators whose income was generated by economy, midscale and upper midscale properties fared much better with lower operational costs and greater occupancy levels.

Impact of COVID and the vaccine on tourism and the economy

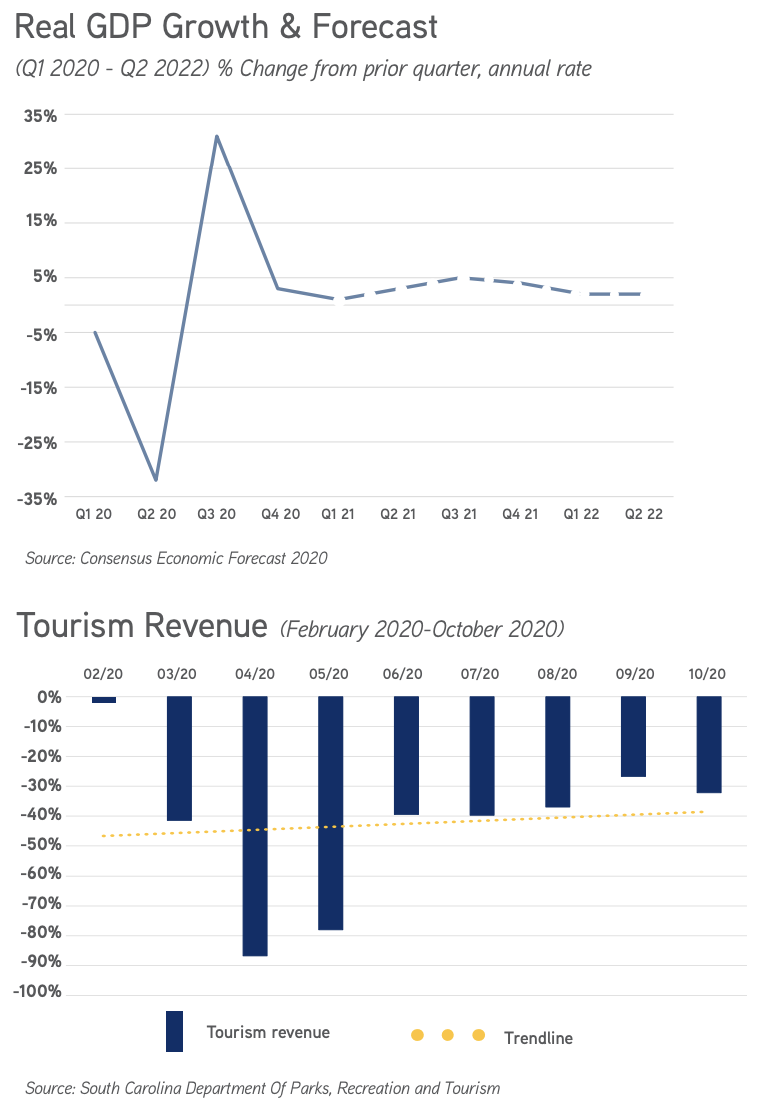

Nearly every metric on the economy and tourism tells a similar story. In April 2020, economic activity dropped substantially. Gross Domestic Product fell 35% in the second quarter, increased 30% in the third quarter and normalized in the fourth quarter at 2%. Going forward, quarterly GDP growth is projected vary between 2% and 4.5% through 2022 according to the Consensus Economic Forecast. Likewise, tourism revenue dropped by 90% in April, and increased to 30% of the normal revenue by October. It is not expected to fully recover until a substantial portion of the population has been vaccinated and the fear of the virus subsides.

Nearly every metric on the economy and tourism tells a similar story. In April 2020, economic activity dropped substantially. Gross Domestic Product fell 35% in the second quarter, increased 30% in the third quarter and normalized in the fourth quarter at 2%. Going forward, quarterly GDP growth is projected vary between 2% and 4.5% through 2022 according to the Consensus Economic Forecast. Likewise, tourism revenue dropped by 90% in April, and increased to 30% of the normal revenue by October. It is not expected to fully recover until a substantial portion of the population has been vaccinated and the fear of the virus subsides.

Hotel income is derived from four sources: business travel, meetings and conventions, food and beverage, and tourism. Business and convention travel has been substantially reduced since April of 2020  when most businesses shifted to a work at home model and increased videoconferencing. The exception to this were business travelers in essential industries that continued to travel although they tended to lodge at properties with interstate access in the economy, midscale and upper midscale sectors. Going forward, it isn’t clear how much business and convention travel demand will recover. Videoconferencing has become ubiquitous across society during the pandemic. It seems likely that many meetings conducted in person will continue using that technology going forward. Convention business will likely recover as the vaccine is deployed and the overall economy recovers.

when most businesses shifted to a work at home model and increased videoconferencing. The exception to this were business travelers in essential industries that continued to travel although they tended to lodge at properties with interstate access in the economy, midscale and upper midscale sectors. Going forward, it isn’t clear how much business and convention travel demand will recover. Videoconferencing has become ubiquitous across society during the pandemic. It seems likely that many meetings conducted in person will continue using that technology going forward. Convention business will likely recover as the vaccine is deployed and the overall economy recovers.

Business in the leisure and hospitality, food and beverage, and entertainment sectors were hardest hit especially in regions with the most stringent government requirements to reduce capacity or close. South Carolina largely lifted these rules by October allowing businesses to function normally. However, consumers have been slow to return to entertainment venues, indoor dining and traveling due to fear of virus exposure.

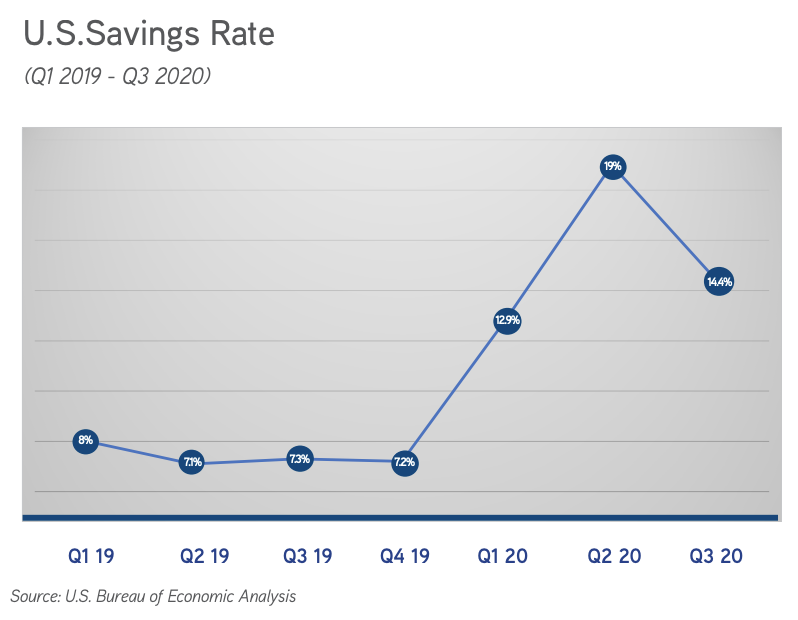

A hopeful metric to watch is the U.S. Savings rate. During the pandemic, household savings increased to a high of 19% as consumer spending on restaurants, entertainment and leisure travel was substantially reduced. By the fall of 2021, households will begin to spend much of this on travel, eating out and entertainment. This should create an enormous boom for businesses serving these sectors. Hotels in tourist dependent markets across all segments should expect increased demand as this materializes.

Hotel Sales

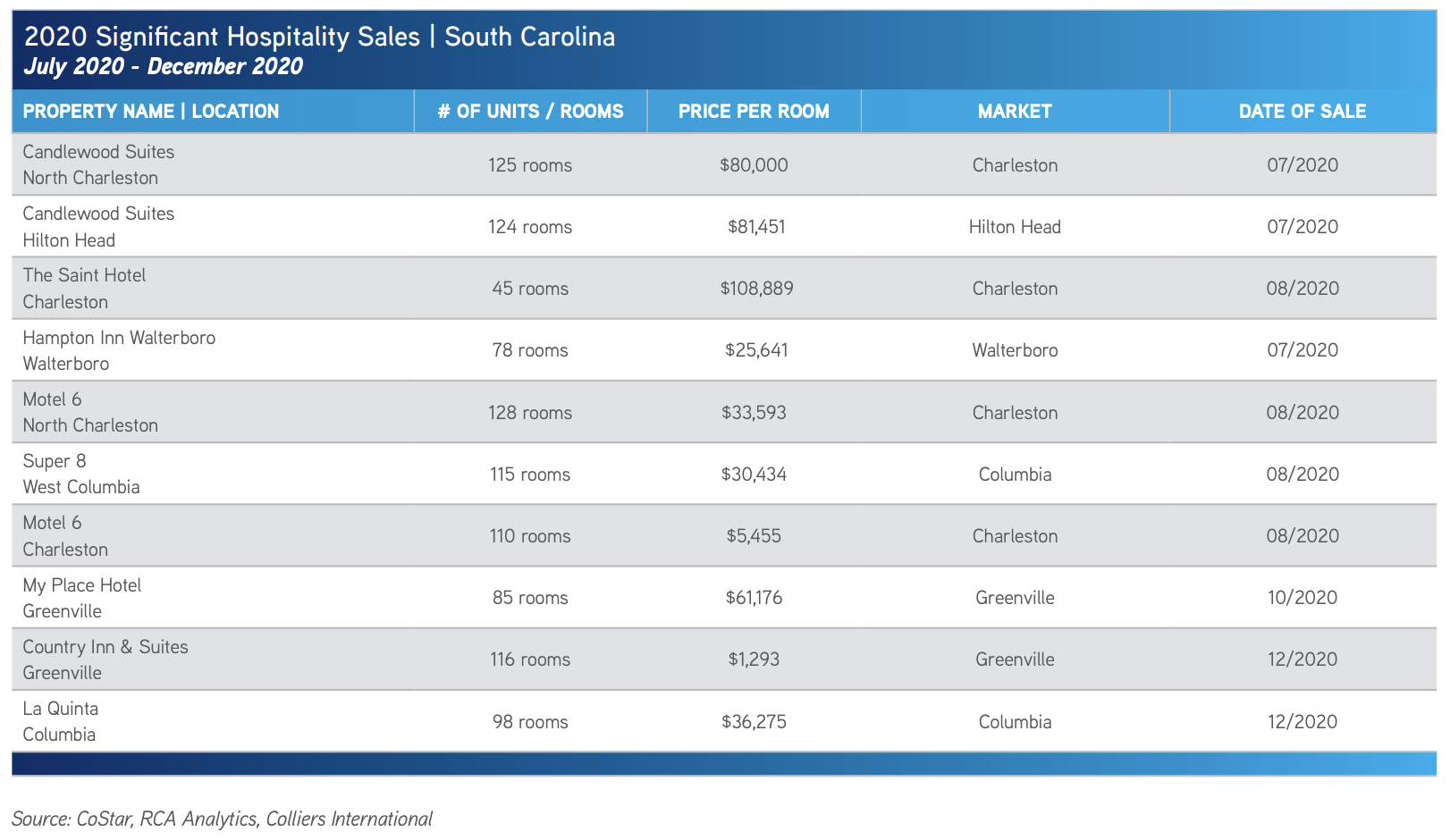

Buyer and sellers were naturally hesitant beginning in April of 2020. In South Carolina, 17 properties traded in 2020 in comparison to the 44 that traded in 2019. Sales were largely limited to properties in the economy, midscale and upper midscale segments with prices between $30,000 and $110,000 a key. As the market stabilizes and improves throughout 2021, we anticipate transactional volume to increase. Savvy proprietors will use this time to rebalance their portfolios to include a larger mix of properties in the most stable product segments and locations. Properties in segments where REVPAR has largely recovered will be in the highest demand as they have proven to best weather the downturn. Additionally, these properties have the lowest operational costs. While the margins may not be as large as more expensive properties, they have generated income throughout the downturn.

Market Forecast

Recovery has arrived in the economy. Hotels in the market, midscale and upper midscale segments in areas like South Carolina that are accessible to much of the U.S. population by car will fare the best. As the vaccine is widely distributed, we expect a substantial tourism boom which should increase occupancies across all segments. Properties catering to business and convention travel will continue to struggle well into 2022 until large numbers of businesses fully return to the workplace and begin planning conventions and meetings.

A Note Regarding COVID-19

As we publish this report, the U.S. and the world at large are facing a tremendous challenge, the scale of which is unprecedented in recent history. The spread of the novel Coronavirus (COVID-19) is significantly altering day-to-day life, impacting society, the economy and, by extension, commercial real estate.

The extent, length and severity of this pandemic is unknown and continues to evolve at a rapid pace. The scale of the impact and its timing varies between locations. To better understand trends and emerging adjustments, please subscribe to Colliers’ COVID-19 Knowledge Leader page for resources and recent updates.

For additional commercial real estate news, check out our market reports here.