LCK Report: Construction starts trending upward after mid-year decline

March 5, 2021

Research & Forecast Report

SOUTH CAROLINA Construction Trends Report Year-end 2020

Key Takeaways

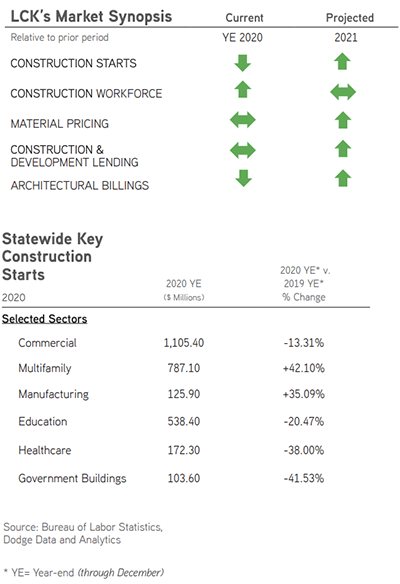

- Year-end statewide construction starts in key sectors are $222 million below 2019 totals. Pre-development indicators appear favorable while the construction workforce exceeds pre-COVID 19 levels. New construction activity began trending upward during the fourth quarter of 2020 after a mid-year decline.

- A decrease in construction starts has led to increased contractor participation and competitiveness. The ability to continue to recognize cost reductions will diminish in 2021 as material pricing remains volatile, material costs are set to escalate, and construction starts increase.

- LCK Construction Tip: The construction market is continuing to feel the medium and long-term implications from the COVID-19 pandemic. As a new normal evolves, owners procuring construction should thoroughly vet prospective contractors before entering into an agreement.

For additional commercial real estate news, check out our market reports here.

Overview

Construction Starts: During 2020, statewide construction starts decreased in four of six sectors as compared to 2019. The two increasing sectors, multifamily and manufacturing, showed a start growth of 42% and 35% respectively for a combined $913 million in new construction projects. Commercial construction starts increased

Construction Starts: During 2020, statewide construction starts decreased in four of six sectors as compared to 2019. The two increasing sectors, multifamily and manufacturing, showed a start growth of 42% and 35% respectively for a combined $913 million in new construction projects. Commercial construction starts increased  significantly during the fourth quarter of 2020, as compared to the preceding three quarters.

significantly during the fourth quarter of 2020, as compared to the preceding three quarters.

Construction Workforce: According to the Bureau of Labor Statistics, as of December 2020, there were 115,000 construction employees in South Carolina, 5,800 more than December 2019. Statewide the construction workforce declined by 6% in April, recouped job losses by September, and now exceeds pre-COVID 19 employment by +/- 5,000 workers.

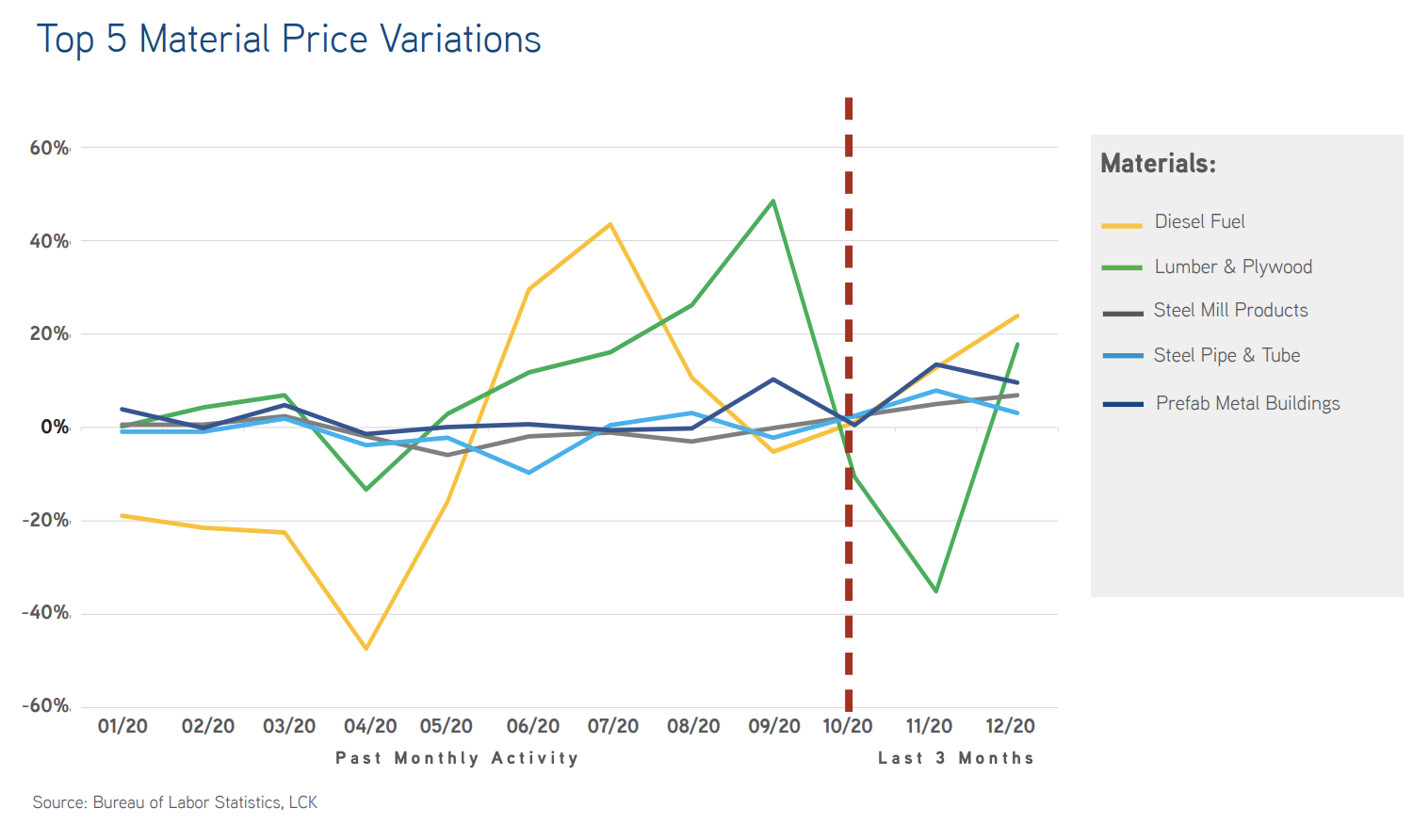

U.S. Material Pricing: A year of pricing stability ended in March 2020 when volatility re-entered the market. Product shortages and price increases for various materials were realized in the spring, while pricing for other materials declined due to decreased demand. The third and fourth quarters of 2020 saw minor upward price movement with average quarterly increases across all materials tallying 2.39% and 1.66%. Diesel fuel, pre-engineered metal buildings, steel products, and precast concrete drove fourth quarter increases. Lumber pricing remains wildly volatile and steel pricing is expected to continue increasing into 2021.

U.S. Construction and Development Lending: According to the FDIC, construction and development loan volume totaled just over $386 billion in the third quarter of 2020, up $26 billion since the third quarter of 2019. The quality of outstanding loans has diminished. Recoveries of delinquent loans declined during 2020 and the net charge-off rate for the third quarter was 0.03%, the highest since the fourth quarter of 2017.

U.S. Architectural Billings: The AIA Billing Index for architects in the south was at a high of 58 in February, bottomed out at 30.6 in May, and then increased month-over-month, ending the year at 46.8. While the index is currently below 50, architects in the south scored highest in the nation in December 2020. (A score of less than 50 indicates decreased billing activity.)

Key Market Summary

Charleston Metropolitan Area

Construction Starts: Charleston’s commercial and education sectors saw a decrease in construction starts in 2020 as compared to 2019. All other major sectors experienced an increase in new construction activity. Commercial starts in November and December, $100 million, suggest optimism after a slow summer and fall. A decline in education starts is not surprising as the Charleston County School District is nearing the end of its Phase IV (2017-2022) Capital Program. The multifamily sector boasted a strong increase in new projects which may be an impetus for future growth in other sectors.

Construction Workforce: The Charleston construction workforce employed 22,000 workers in December 2020, a 1.19% increase over the past year. A loss of 1,400 workers occurred in April 2020, 1,000 of which were recovered by year-end.

Columbia Metropolitan Area

Construction Starts: Three major sectors in the Columbia market; multifamily, manufacturing, and education, saw an uptick in construction starts during 2020. Starts in the commercial, healthcare, and government buildings sectors were down. Education starts in 2020 totaled $209 million due to public school building programs underway in Lexington School District 1 and Richland School District 2. Interestingly, 66% of all multifamily starts began in August and November, noteworthy because no multifamily work began between March and June. Sitework for a significant beverage manufacturing facility began in late 2020. This single project will have a major impact on 2021 construction starts in the Columbia market.

Construction Workforce: The Columbia construction workforce totaled 18,200 workers in December 2020, a 4.6% increase over the past year. A workforce reduction of 9.25% occurred in April 2020 with rebounds in May and June making up for April losses. At year-end, the Columbia construction workforce exceeded pre-COVID 19 levels.

Greenville-Anderson-Mauldin Metropolitan Areas

Construction Starts: Contrary to other key markets, Greenville’s commercial sector showed an increase in new projects as compared to 2019. The multifamily, manufacturing, and healthcare sectors also grew, while new projects decreased in the education and government buildings sectors. Lower starts in the government buildings sector is expected as a large federal courthouse project began in 2019. A reduction in education starts is not a surprise as the sector is cyclical.

Construction Workforce: The Greenville construction market employed 19,500 workers in December 2020, an 1.12% increase over the past year. A loss of 600 workers occurred in April. Like Columbia, all losses were reversed by June and at year-end Greenville’s construction workforce surpassed pre-COVID 19 employment.

Spartanburg Metropolitan Area

Construction Starts: The Spartanburg market has realized $121 million in multifamily construction starts and $20 million in new manufacturing projects during 2020, up sharply from starts in 2019. The majority of multifamily starts occurred during the first half of 2020 with little work occurring during the second half of the year. Construction in this market is being fueled by the single-family residential sector. Continued home building along with increased multifamily and manufacturing starts can be expected to drive project growth across the remaining sectors. Advantageous construction pricing is likely to be realized in the Spartanburg market.

Construction Forecast

During 2020, South Carolina’s construction market faced an array of difficulties from postponed projects to material procurement challenges and workforce safety concerns. Despite the unknown and the unprecedented, the South Carolina construction industry quickly adapted to a new normal. The turning point was the third quarter of 2020 when statewide construction workforce losses throughout the first and second quarters were first regained, and then exceeded pre-COIVD construction employment. Likewise, architectural billings, a predictor of future work, began increasing in the third quarter after hitting second quarter lows. During the fourth quarter, new commercial construction projects totaled $484 million, the highest quarterly total since the first quarter of 2019 and more than double individual quarterly totals for Q1-Q3 of 2020.

The industry’s outlook for 2021 remains apprehensively optimistic with some losses expected. Pre-development indicators are favorable and increased fourth quarter 2020 starts have maintained the workforce. Demand for distribution and warehouse construction remains high which has resulted in rising steel prices. Increased healthcare work is anticipated as postponed capital projects restart, and new hospitals are expected in York and Horry counties. Increased contractor participation and material pricing increases can be expected into 2021. If construction starts increase and backlog is replenished, the market could once again favor contractors.

LCK provides professional project management solutions which enable clients to effectively leverage these statistics to position their project for development. Through creative procurement strategies, cost-management practices, and return on investment analysis, LCK utilizes its professional resources to deliver the most affordable projects to its clients. Attentive, hands-on management at every step results in successful developments delivered on time and on budget.

For additional commercial real estate news, check out our market reports here.