LCK Report: South Carolina Construction Starts and Costs are Rising

September 15, 2021

Research & Forecast Report

2021 SOUTH CAROLINA | CONSTRUCTION TRENDS

Key Takeaways

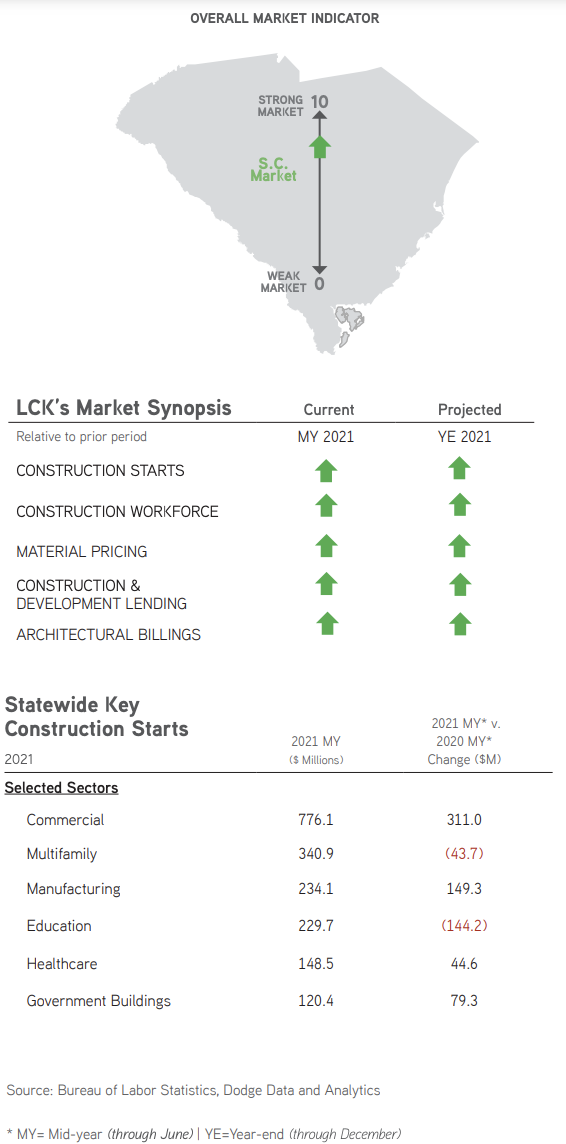

- Mid-year statewide construction starts in key sectors totaled $1.85B, a $426M increase compared to mid-year 2020. Pre-development indicators, particularly architectural billings, appear favorable for future growth.

- An increase in construction starts paired with steep material price increases resulted in rising construction costs. Prolonged material lead times are delaying the start of some projects. Suppliers, particularly those of steel joists and metal deck, are holding pricing for negligible periods of time. These pressures may diminish an otherwise optimistic market outlook.

- LCK Construction Tip: Plan well, get creative and start early. Alternative construction methods, accelerated design and strategic procurements are necessary to control costs and maintain conventional project delivery timelines.

Overview

Overview

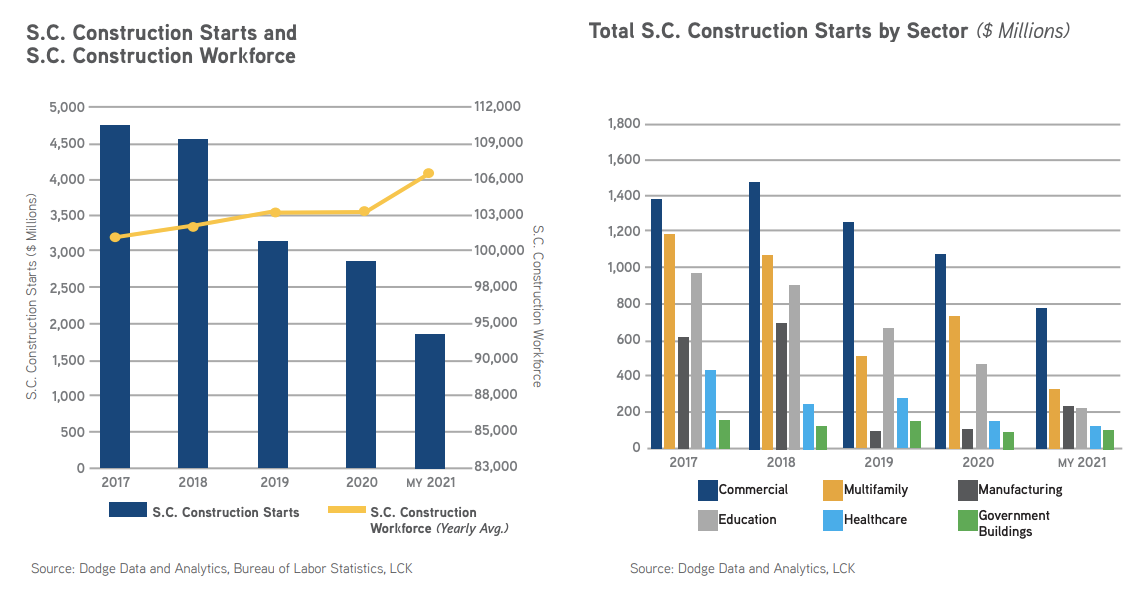

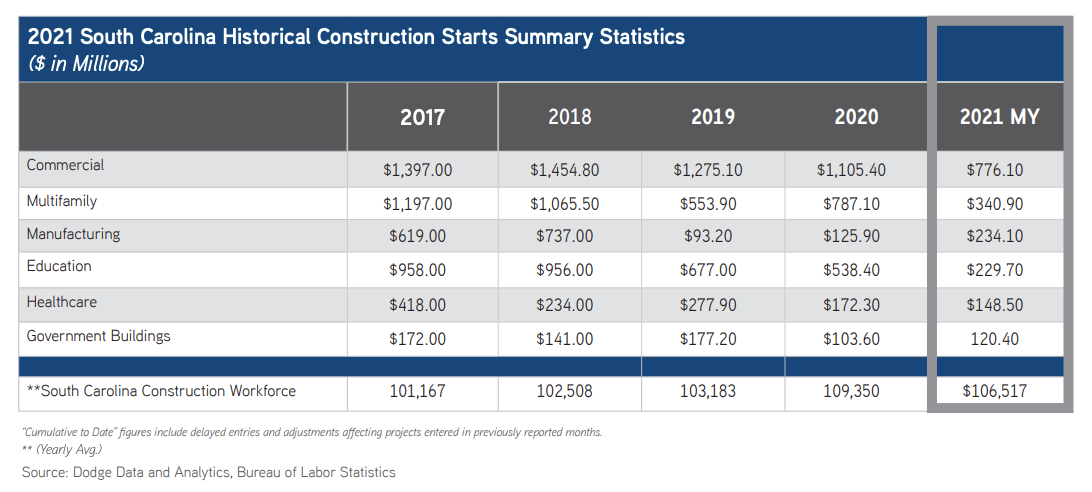

Construction Starts: Statewide construction starts have increased in four of six sectors as compared to mid-year 2020. Commercial and manufacturing starts for the first six months of 2021 total over $1B dollars with commercial starts increasing in all key markets. A drop in education starts is not concerning as the sector is cyclical and South Carolina’s population continues to increase which will impact those starts over time.

Construction Workforce: According to the Bureau of Labor Statistics, as of June 2021 construction employment in South Carolina totaled 107,000 persons, 4,900 more than June 2020 and roughly 300 more than pre-pandemic first quarter 2020 averages. South Carolina’s unemployment rate continues to decrease with June at 4.5%, lower than the national average of 7.5%.

U.S. Material Pricing: Material pricing is volatile and increasing. Demand, supply chain distributions, and workforce shortages amongst producers are all contributing factors. Three-month pricing index averages from April thru June 2021 increased for eighteen of nineteen tracked materials. Seven of these materials saw increases above 10%. The highest increases were recognized in lumber at +30.2%, all types of steel and metal products at +10.6% to +25.4%, and gypsum products at +11.0%. Lower price increases for other materials would have made the top five list in prior publications of this report. Lumber costs have started to decrease, albeit from an elevated position. It remains unclear if steel and metal products have hit a price ceiling.

U.S. Construction and Development Lending: According to the FDIC, construction and development loan volume totaled $388 billion in the first quarter of 2021, up $18 billion since the first quarter of 2020. The quality of outstanding loans is declining, although slightly, with increases to the noncurrent rate in every quarter since the first quarter of 2020. The first quarter 2021 noncurrent rate is 0.72%, the highest since the fourth quarter of 2016.

U.S. Architectural Billings:The AIA Billing Index for architects in the south has risen from 47.4 in January 2021 to 57.3 in June 2021. Since March 2021 all regions have reported monthly index scores above 50 indicating a robust nationwide pipeline for future construction starts. (A score of less than 50 indicates decreased billing activity.)

Key Market Summary

Charleston Metropolitan Area

Construction Starts: The Charleston market recorded $622M of commercial, multifamily, and government building starts during the first half of 2021, a $268M increase as compared to the first six months of 2020. Education and healthcare construction starts were $65M over the same period, a $60M decrease in construction as compared to mid-year 2020.

Construction Workforce: The Charleston-North Charleston construction workforce has 21,300 workers, a 2.4% increase over the past year.

Columbia Metropolitan Area

Construction Starts: Starts in the Columbia market across selected sectors from January thru June of this year totaled $519M. The manufacturing sector led the way with $200M in starts followed by $174M of education construction and $126M of commercial construction starts. Each of these sectors showed significant growth as compared to mid-year 2020. Multifamily and healthcare starts are down compared to last year while government building starts remain consistent.

Construction Workforce: The Columbia construction workforce has 18,500 workers accounting for a 7.56% increase in construction employment over the past twelve months.

Greenville-Anderson-Mauldin Metropolitan Areas

Construction Starts: The Greenville market realized $247M in construction starts across selected sectors as of June 2021, a $105M increase compared to mid-year 2020. The commercial and multifamily sectors realized sizeable starts growth of $96M and $57M respectively. Manufacturing starts are down by $45M compared to the first half of 2020. The education and healthcare sectors have seen comparatively few starts during mid-year 2021 and 2020.

Construction Workforce: The Greenville-Anderson-Mauldin construction workforce accounts for 20,500 workers, a 5.76% increase over the past twelve months.

Spartanburg Metropolitan Area

Construction Starts: Selected market sectors in Spartanburg saw $125M in construction starts during the first half of 2021. The commercial sector led the way with $105M in new projects started. Mid-year 2021 starts are stable on a comparative basis coming in $4M higher than mid-year 2020 starts. A $101M increase in commercial starts counterbalanced a $96M decrease in multifamily starts. Small changes, both up and down, were realized across the other sectors.

Construction Forecast

All indicators signal South Carolina’s construction market, and possibly the national market, have recovered from disruptions brought about by the COVID-19 pandemic in early to mid-2020. Along with the recovery, unprecedented material price increases have been experienced during the first half of 2021. Market shifts accelerated by COVID-19, particularly a fast-tracked move to e-commerce, have increased demand for key materials beyond supply and domestic production capabilities. Pressure has mounted on procurers of construction as costs have risen, prices are held for negligible periods of time, and increasing lead-times have delayed the start of projects. Supply chain shortcomings are challenged by workforce shortages, further compounding delays in product deliveries.

The industry’s outlook for the remainder of 2021 remains mixed. Increases in construction lending and architectural billings suggest a strong project pipeline. Workforce growth continues but may exert upward pressure on prices as demand has been growing at a faster pace. If material cost increases persist and lead-times continue to threaten schedules, some owners may determine development projects are not a viable or strategic option. The continuation of the COVID-19 pandemic remains a wild card of uncertainty. Price increases and prolonged schedules should be expected for the remainder of 2021.

LCK provides professional project management solutions which enable clients to effectively leverage these statistics to position their project for development. Through creative procurement strategies, cost-management practices, and return on investment analysis, LCK utilizes its professional resources to deliver the most affordable projects to its clients. Attentive, hands-on management at every step results in successful developments delivered on time and on budget.

For additional commercial real estate news, check out our market reports here.

To download the complete report: 2021 Construction Trends South Carolina Report