Colliers Report: South Carolina’s industrial market expands to accommodate ongoing demand

February 4, 2020Research & Forecast Report

Q4-2019 SOUTH CAROLINA | INDUSTRIAL

Key Takeaways

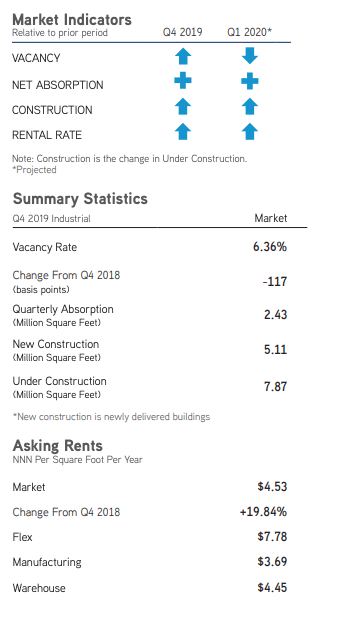

- A record-breaking 15.88 million square feet of industrial buildings were delivered throughout South Carolina in 2019; however, the vacancy rate still dropped 117 basis points from the fourth quarter of 2018 through year-end 2019.

- During the calendar year 2019, the South Carolina Ports Authority reached a record-breaking container volume.

2019 Industrial Annual Recap

2019 Industrial Annual Recap

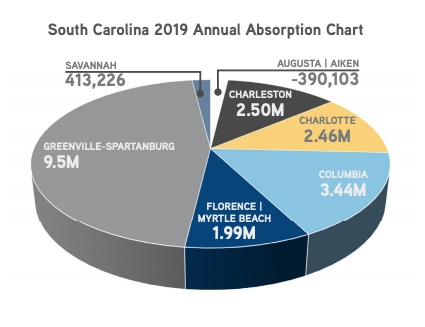

During 2019, the South Carolina industrial market grew significantly- there were 77 new industrial buildings delivered to the market adding 15.88 million square feet, and there are currently 8.33 million square feet under construction. In addition, another 5.83 million square feet of industrial buildings are proposed to be built statewide. In addition to a record number of building deliveries during 2019, the South Carolina industrial market absorbed 20.03 million square feet. Therefore, the market vacancy rate dropped 117 basis points from the fourth quarter of 2018 down to 6.36% during this quarter. The overall average South Carolina industrial weighted rental rate rose from $3.78 per square foot during the fourth quarter of last year to $4.53 per square foot during the fourth quarter of 2019.

Quarterly Market Overview

The South Carolina industrial market is comprised of 442.03 million square feet within 6,935 buildings. From the third quarter through the fourth quarter of this year, the South Carolina market grew by twenty buildings which added approximately 5.11 million square feet. Due to the delivery of new industrial construction, the overall South Carolina market vacancy rate increased from 5.82% last quarter to 6.36% during the fourth quarter of this 2019. The South Carolina industrial markets absorbed approximately 2.43 million square feet during the fourth quarter of 2019 – the Greenville-Spartanburg market absorbed the most with 1.78 million square feet followed by the Columbia market with 1.11 million square feet of absorption. The average triple net South Carolina market rental rate for the remaining available industrial space increased to $4.53 per square foot this quarter.

The South Carolina industrial market is comprised of 442.03 million square feet within 6,935 buildings. From the third quarter through the fourth quarter of this year, the South Carolina market grew by twenty buildings which added approximately 5.11 million square feet. Due to the delivery of new industrial construction, the overall South Carolina market vacancy rate increased from 5.82% last quarter to 6.36% during the fourth quarter of this 2019. The South Carolina industrial markets absorbed approximately 2.43 million square feet during the fourth quarter of 2019 – the Greenville-Spartanburg market absorbed the most with 1.78 million square feet followed by the Columbia market with 1.11 million square feet of absorption. The average triple net South Carolina market rental rate for the remaining available industrial space increased to $4.53 per square foot this quarter.

Augusta | Aiken (South Carolina portion)

The South Carolina portion of the Augusta | Aiken market is comprised of 13.59 million square feet, over half of which is manufacturing space. No new industrial buildings were delivered to this market; however, the 40,000-square-foot AmbioPharm expansion continued construction. The Augusta | Aiken market absorbed 7,400 square feet during the fourth quarter of 2019 within two warehouses. There was no activity in the Flex/R&D sector, nor in the manufacturing sector during the fourth quarter of 2019. Consequently, the overall market vacancy rate decreased minimally from 15.68% during the third quarter of this year to 15.61% during the fourth quarter. The average weighted rental rate for the South Carolina portion of the Augusta | Aiken region decreased from $2.99 per square foot during the third quarter to $2.61 per square foot at year-end.

Charleston

The Charleston industrial market has 57.20 million square feet of industrial inventory with approximately 2.82 million square feet under construction within 13 buildings. In addition, there are approximately 13 buildings proposed to be built within the Charleston market which would add an additional 3.84 million square feet to the industrial inventory. There were five new buildings delivered to the market this quarter which added 867,783 square feet to the Charleston industrial inventory. The Charleston industrial market absorbed 453,503 square feet during the fourth quarter of 2019. Due to the large amount of construction delivery during the fourth quarter of 2019, the overall Charleston vacancy rate increased from 8.25% during the third quarter of 2019 to 8.87% this quarter. The overall market average triple net weighted rental rate increased this quarter to $6.03 per square foot.

Charlotte (South Carolina portion)

The South Carolina portion of the Charlotte submarket has an industrial inventory totaling 39.74 million square feet, and there are currently 458,052 square feet of warehouse space currently under construction. Two warehouses and one flex building delivered to the Charlotte market during the fourth quarter of 2019 adding 390,372 square feet to the inventory in York County and all but 25,000 square feet of the new space was absorbed. However, the South Carolina portion of the Charlotte market still posted a negative absorption of 25,930 square feet during the fourth quarter of 2019. As a result, the overall quarterly market vacancy rate increased from 6.81% last quarter to 7.72% at year-end. Average weighted rental rates for the remaining industrial space decreased from $5.41 per square foot during the third quarter of 2019. to $5.24 per square foot this quarter.

Columbia

The Columbia industrial market is comprised of 72.51 million square feet. During the fourth quarter of 2019, the market absorbed 956,603 square feet, over half of which was absorbed within the warehouse sector. Orangeburg County was the submarket with the highest absorption of 417,817 square feet, followed by Northeast Columbia with 209,500 square feet of absorption. There is currently one building under construction which, upon completion, will add 65,000 square feet to the market. Two buildings were delivered to the market during the fourth quarter of 2019 adding 270,000-square-foot to the Columbia market. The quarterly vacancy rate dropped from 5.48% during the third quarter of 2019 to 4.52% at year-end. The overall average market rental rate for available industrial space rose from $3.95 per square foot during the third quarter of 2019 to $4.03 per square foot at the end of 2019.

Florence | Myrtle Beach

The Florence | Myrtle Beach market is comprised of 38.28 million square feet of industrial properties and posted a negative absorption of 903,684 square feet during the fourth quarter of 2019. The negative absorption was almost split equally between warehouse and manufacturing space. No new buildings were delivered to the market during the fourth quarter of 2019, but construction continues on two warehouses which, upon completion, will add 309,400 square feet to the market. Due to the negative absorption, the vacancy rate increased to 7.44% and the overall Florence | Myrtle Beach weighted rental rates decreased to $2.68 per square foot this quarter.

Greenville-Spartanburg

Comprised of approximately 210.76 million square feet, there are currently 3.99 million square feet among 17 buildings under construction and 15 additional proposed properties totaling 1.92 million square feet delivering throughout the Greenville-Spartanburg market. During the fourth quarter of 2019, 3.56 million square feet of industrial buildings were delivered and 1.78 million square feet were absorbed. Subsequently, the quarterly market vacancy rate increased from 4.59% to 5.36%.

Savannah (South Carolina portion)

The Savannah market within South Carolina has 10.32 million square feet of industrial space and absorbed 20,739 square feet during the fourth quarter of 2019 – the manufacturing sector absorbed 113,230 square feet this quarter; however, the warehouse sector posted a net negative absorption of 112,991 square feet. There is one 17,500-square-foot warehouse under construction and one 22,500-square-foot flex/R&D building delivered to the market during the fourth quarter of 2019. The overall quarterly vacancy rate remained at 5.66% this quarter and the average triple net weighted rental rate increased to $5.20 per square foot.

Significant Transactions

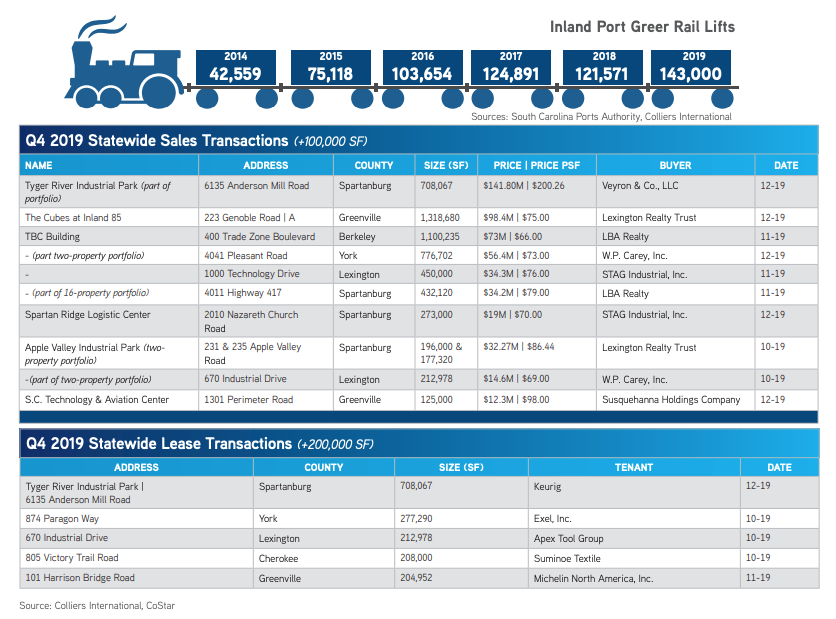

There were 120 industrial sale transactions reported through CoStar during the fourth quarter of 2019 to include a $141.80 million, seven-property portfolio sale including a building within the Tyger River Industrial Park. There were 89 leases executed during the fourth quarter of 2019. Several sales involved sale-leaseback transactions.

South Carolina Ports

According to a 2019 economic impact study conducted by the University of South Carolina Darla Moore School of Business, the South Carolina Ports Authority is responsible for 224,963 jobs across South Carolina, or one in every 10 jobs; 52% of this impact is concentrated in the Upstate. In 2019, the South Carolina ports system produced $63.4 billion in annual economic impact, generated more than $12.8 billion in labor income and $1.1 billion in annual tax revenue.The S.C. Ports Authority had its best calendar year in the history of its operations. There was a 5% increase year-over-year from 2018 to 2019 and the ports handled 2.44 million twenty-foot equivalent container units (TEUs). In addition, the Inland Port Dillon and Inland Port Greer also increased activity by 41% from 2018 to 2019, breaking previous records with a 190,539 combined rail moves.The South Carolina Ports Authority President and CEO Jim Newsome stated,“We enter 2020 with a great decade of growth behind us, during which we doubled our volumes, tripled our asset base and added more than 200 people to our team. Our cargo growth and efficient terminals are only made possible through the dedication of our team and the broader maritime community.”According to the South Carolina Ports Annual Report, by 2021 the first phase of the Leatherman terminal is set to open and the Wando terminal will have 15 155-foot-tall ship-to-shore cranes with the ability to manage three 14,000-TEU ships concurrently.

Market Forecast

The South Carolina industrial market will benefit from the recently negotiated U.S.-China Trade Deal and USMCA. The two most pertinent aspects of the deal affecting South Carolina industrial markets promote increased purchases of American products and tariff relief on Chinese products. These changes will lead to an increase in imports and exports. The Port of Charleston is already performing exceedingly well, reporting record-breaking numbers in 2019. Since the Port of Charleston is the gateway to the South Carolina logistics pipeline, the demand for industrial space will continue to climb through 2020. An expansive industrial pipeline is expected to deliver in the next few quarters and be quickly absorbed due to increasing statewide industrial demand. Average rental rates are on the rise due to high-quality new buildings forcing the rent upward.

For additional commercial real estate news, check out our market reports here.